Get This Report on Hsmb Advisory Llc

Plan advantages are minimized by any type of superior lending or finance interest and/or withdrawals (Health Insurance St Petersburg, FL). Rewards, if any, are affected by plan fundings and finance passion. Withdrawals above the expense basis might result in taxed regular revenue. If the plan gaps, or is surrendered, any kind of superior lendings thought about gain in the policy might go through regular earnings tax obligations.

If the plan owner is under 59, any taxed withdrawal might likewise be subject to a 10% government tax fine. Cyclists might incur an added expense or premium. Riders might not be readily available in all states. All entire life insurance policy policy guarantees go through the timely settlement of all called for premiums and the cases paying ability of the releasing insurance policy business.

The money surrender worth, finance value and fatality proceeds payable will be reduced by any kind of lien exceptional as a result of the repayment of an increased benefit under this biker. The increased benefits in the initial year reflect reduction of a single $250 management fee, indexed at a rising cost of living price of 3% annually to the rate of acceleration.

Not known Incorrect Statements About Hsmb Advisory Llc

A Waiver of Premium motorcyclist forgoes the responsibility for the insurance holder to pay more costs need to she or he become completely handicapped constantly for at the very least six months. This biker will sustain an extra expense. See policy contract for additional details and needs.

Here are numerous cons of life insurance policy: One negative aspect of life insurance policy is that the older you are, the more you'll spend for a policy. This is because you're more most likely to die throughout the plan period than a younger insurance policy holder and will, subsequently, cost the life insurance policy company even more cash.

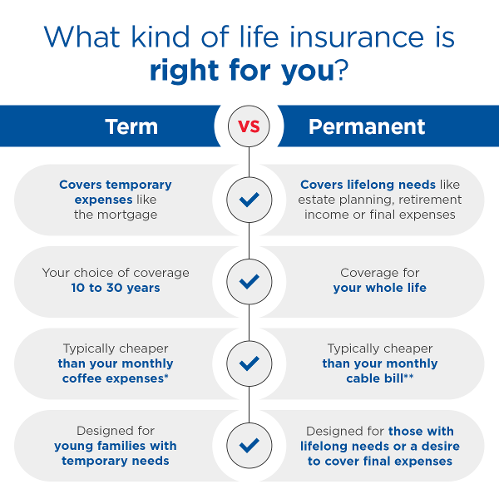

2 If you select a permanent life plan, such as whole life insurance policy or variable life insurance, you'll receive lifelong protection. 2 If you're interested in life insurance, think about these ideas:3 Do not wait to use for a life insurance coverage plan.

Some Known Facts About Hsmb Advisory Llc.

By making an application for life insurance policy protection, you'll be able to assist safeguard your enjoyed ones and gain some comfort. Aflac's term and entire life insurance policy policies can provide you comprehensive coverage, premiums that fit most budget plans, and various other advantages. If you're unsure of what kind of insurance coverage you should obtain, speak to an agent to discuss your choices - St Petersburg, FL Life Insurance.

There are many potential benefits of life insurance policy however it's normally the peace of mind it can provide that matters the most - https://lwccareers.lindsey.edu/profiles/4506780-hunter-black. This is because a payout from life cover can serve as a financial safety and security net for your loved ones to draw on need to you pass away while your plan is in area

But the bypassing benefit to all is that it can eliminate a minimum of one fear from those you appreciate at a tough time. Life insurance policy can be set up to cover a home loan, possibly helping your family members to stay in their home if you were to pass away. A payout could help your dependants replace any kind of revenue shortfall really felt by the loss of your earnings.

Unknown Facts About Hsmb Advisory Llc

A payout could be utilized to help cover the price of your funeral. Life cover can help mitigate if you have little in the means of savings. Life insurance policy items can be used as part of estate tax preparation in order to reduce or prevent this tax obligation. Placing a policy in trust can offer higher control over possessions and faster payouts.

You're hopefully removing a few of the anxiety felt by those you leave behind. You have comfort that enjoyed ones have a particular degree of financial protection to draw on. Taking out life insurance to cover your home mortgage can give satisfaction your home loan will certainly be repaid, and your liked ones can continue living where they have actually constantly lived, if you were to pass away.

The 8-Second Trick For Hsmb Advisory Llc

Arrearages are usually repaid utilizing the worth of an estate, so if a life insurance policy payment can cover what you owe, there ought to be extra delegated hand down as an inheritance. According to Sunlife, the typical price of a basic funeral service in the UK in 2021 was simply over 4,000.

Getting The Hsmb Advisory Llc To Work

It's a considerable sum of money, but one which you can give your loved ones the opportunity to cover making use of a life insurance coverage payout. You ought to get in touch with your provider on details of how and when payouts are made to make sure the funds can be accessed in time to spend for a funeral service.

It might also provide you much more control over who gets the payout, and help in reducing the possibility that the funds might be made use of to pay off financial obligations, as could happen if the plan was beyond a trust. Some life insurance policy policies consist of an incurable ailment advantage choice at no additional expense, which could result in your policy paying early if you're identified as terminally unwell.

A very early repayment can allow you the possibility to obtain your affairs in order and to take advantage of the moment you have left. Losing someone you love is difficult enough to manage by itself. If you can assist minimize any worries that those you leave may have about just how they'll cope financially moving on, they can concentrate on the points that really need click over here to matter at the most tough of times.